/cloudfront-us-east-2.images.arcpublishing.com/reuters/JEUL2B5V7BJCFMRTKGOS3ZSN4Y.jpg "Hungary’s anti-LGBTQ law breaches international rights standards – European rights body")

/cloudfront-us-east-2.images.arcpublishing.com/reuters/DYF5BFEE4JNPJLNCVUO65UKU6U.jpg "The curious case of a map and a disappearing Taiwan minister at U.S. democracy summit")

/cloudfront-us-east-2.images.arcpublishing.com/reuters/UF7R3GWJGNMQBMFSDN7PJNRJ5Y.jpg "Blinken touts deeper U.S. engagement amid concern over ‘aggressive’ China")

United States:

Profitability threshold

August 02, 2021

Mayer Braun

To print this article, all you need to do is register or log in to Mondaq.com.

On April 15, 2020, the OECD published the report entitled “Tax and Tax Policies in Response to the Coronavirus Crisis: Building Confidence and Resilience” (the “COVID-19 Response”). The COVID-19 response discussed the crucial steps many governments have taken to contain and contain the spread of the virus and limit the negative impact on their citizens and their economies, and outlined various tax policy options as available tools. The obligation to respond to the tax challenges of the digitization of the economy and to ensure that MNEs pay a minimum tax level is included in the tax policy discussion. (P.6) In the COVID-19 environment, the new impetus for efforts to reach an international agreement on issues relating to the first pillar can now not only come from “[t]he increased use of digital services “, but also from” the need to generate more income “, which can be achieved in part by” strengthening the taxation of economic rents “(p.6), especially for companies that were exposed during the crisis.

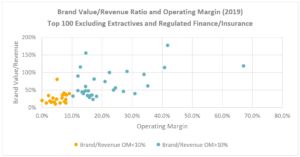

The intention to focus the “taxation of economic rents” on higher-performing companies was confirmed in the OECD’s “Declaration on a two-pillar solution for overcoming the tax challenges posed by the digitization of the economy” published on July 1, 2021 that companies falling within the scope are defined as MNEs with a worldwide turnover of over 20 billion euros and a profitability of over 10%. While the profit margin cut-off may seem reasonable, the one-size-fits-all approach is daunting.

A brief overview of the top 100 brands that were rated by BrandFinance1 clarifies the point: While for companies with an operating margin below 10%, the ratio of brand value to sales is between around 15% – which companies as suggested in the declaration Scope of application would fall – the ratios of brand value to sales are widely spread between 20% and over 100%. So if the profitability of 10% were accepted as a simple mechanical threshold, the residual profits that would be allocated as amount A could include, in part, the return of the MNE brands. Whether this is the intention of the OECD is doubtful.

footnote

1 branddirectory.com/global Brand Finance Global 500 January 2020

Visit us at mayerbrown.com

Mayer Brown is a global legal services provider that includes law firms that are separate entities (the “Mayer Brown Practices”). The Mayer Brown Practices are: Mayer Brown LLP and Mayer Brown Europe – Brussels LLP, both Limited Liability Partnerships based in Illinois, USA; Mayer Brown International LLP, a Limited Liability Partnership incorporated in England and Wales (authorized and regulated by the Solicitors Regulation Authority and registered in England and Wales under number OC 303359); Mayer Brown, a SELAS founded in France; Mayer Brown JSM, a Hong Kong partnership and its affiliates in Asia; and Tauil & Checker Advogados, a Brazilian law firm affiliated with Mayer Brown. “Mayer Brown” and the Mayer Brown logo are trademarks of Mayer Brown Practices in their respective jurisdictions.

© Copyright 2020. The Mayer Brown Practices. All rights reserved.

This article by Mayer Brown contains information and commentary on legal issues and developments of interest. The foregoing does not constitute a comprehensive treatment of the subject under discussion and is not intended as legal advice. Readers should seek specific legal advice before taking any action in relation to the matters discussed here.

POPULAR ARTICLES ON: United States Taxes

{kind=link}